KWSP Dividend Calculation Explained: How Your 2025 6.15% Dividen is Actually Computed (MADB Method)

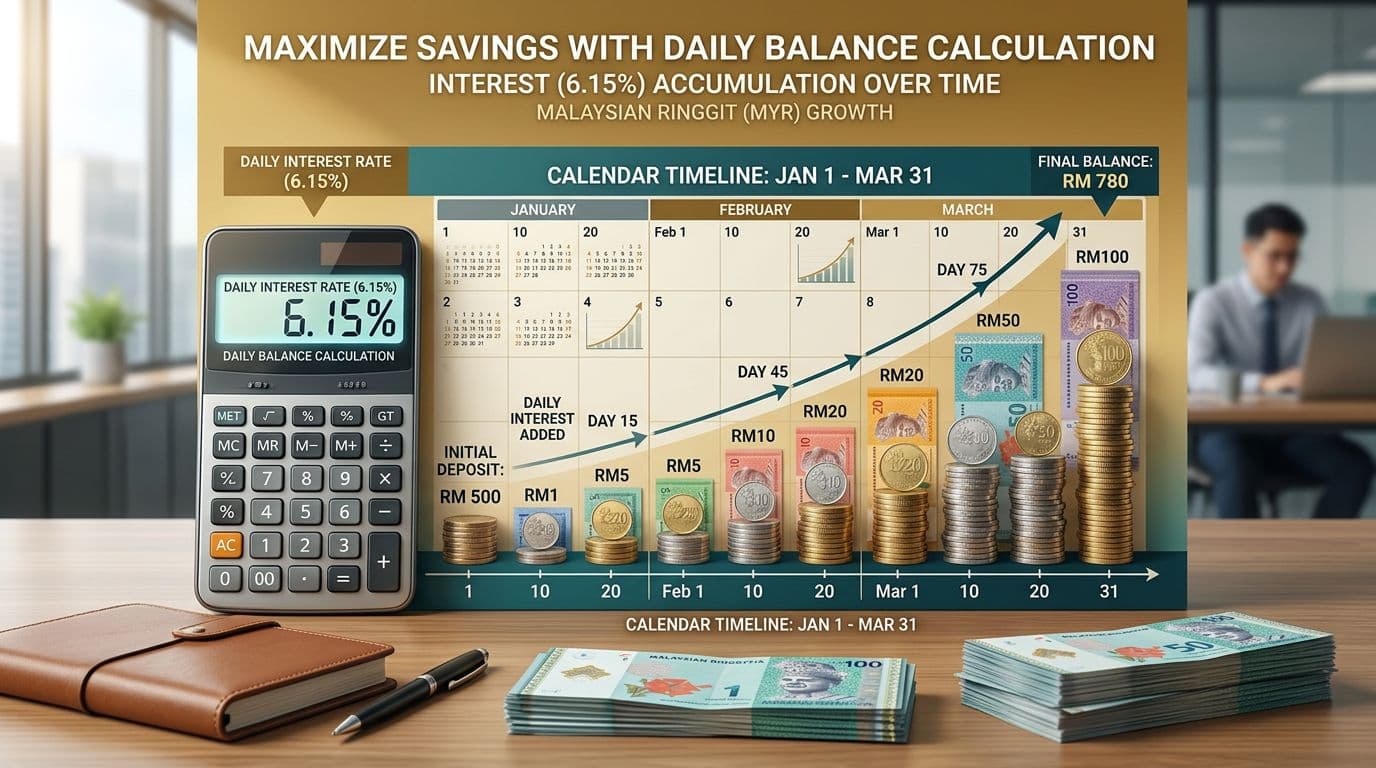

KWSP does not calculate your dividend by multiplying your year-end balance by 6.15%. It uses the Modified Aggregate Daily Balance (MADB) method so each ringgit earns based on time in the account.

How KWSP Decides the 6.15% Rate (Big Picture)

EPF invests your savings across stocks, bonds, property, infrastructure, and other asset classes. After deducting management expenses and setting aside reserves, KWSP divides net profit by total members' savings to arrive at the declared dividend rate. For 2025, that rate is 6.15%, well above the 2.50% minimum guarantee for Conventional savings — see the full KWSP Dividen 2026 announcement breakdown for payout details and i-Akaun steps.

How Your Personal Dividend is Calculated: MADB in Simple Terms

KWSP looks at your daily balance throughout the entire year from 1 January to 31 December 2025. The dividend is computed using the Modified Aggregate Daily Balance (MADB) concept, whereby the contributions for a particular month are eligible for dividends from the last day of the contribution month until 31 December 2025.

Key Rules of MADB

These rules explain how KWSP computes your dividend:

- Your opening balance on 1 January 2025 earns the full 365 days of dividend.

- Every contribution (employer, employee, voluntary i-Simpan) starts earning dividend only from the last day of the month it is credited.

- Withdrawals reduce your balance immediately, so you lose dividend on the withdrawn amount for the remaining days of the year.

- Everything is calculated daily, then totalled and credited on 1 March 2026.

Real-Life Example: RM1,000 Monthly Contribution, No Withdrawals

Assume you started 2025 with RM10,000 and contributed RM1,000 every month for a total of RM12,000 in contributions. Your opening RM10,000 earns dividend for 365 days, which works out to approximately RM615. The January contribution of RM1,000 earns from 31 January for 335 days, approximately RM56.60. February earns from 28 February for 306 days, approximately RM51.70. Each subsequent month earns fewer days.

By the time you reach the December contribution, it earns one day of dividend, roughly RM0.17. Your total estimated dividend for the year would be approximately RM956, bringing your year-end balance to around RM22,956. The actual amount in your i-Akaun is calculated to the sen using the exact daily method.

What If You Made Withdrawals?

Every time you withdraw from Akaun Fleksibel, Sejahtera, or Persaraan, that amount stops earning dividend from the withdrawal date onward. KWSP shows separate dividend figures for each account in your Member Statement. Withdrawals reduce your balance and the dividend you earn for the rest of the year.

Pro Tips to Maximise Your KWSP Dividend

These steps help you get more out of the MADB system:

- Contribute early in the year because January and February contributions earn almost a full year of dividend.

- Avoid withdrawals from your main retirement accounts unless you need the money.

- Voluntary top-ups via i-Simpan still get full benefit even if credited later in the month, as long as it counts for that contribution month.

- Late employer contributions? You still get dividend backdated to the original month because KWSP tracks this automatically.

How to See Your Exact Breakdown Right Now

Your full dividend breakdown is available via i-Akaun from 1 March 2026:

- Open the KWSP i-Akaun app (updated version).

- Go to Member Statement and select 2025.

- You will see your opening balance on 1 January 2025, monthly contributions and withdrawals, and the exact dividend credited for each Akaun (Persaraan, Sejahtera, Fleksibel).

- The total dividend for 2025 is displayed at the bottom of the statement.

Interim Dividend for Early 2026 Withdrawals

If you withdraw fully, for example at age 55 or 60, between 1 January and the actual crediting date, KWSP pays a 2.50% interim dividend first, then tops up the difference to the declared rate of 6.15% within approximately one week. This prevents members who exit early from losing out while waiting for the official declaration.

Start Contributing Smart Today

Every early ringgit grows longer under the MADB system. When you understand how KWSP calculates your dividend, you can make better decisions about contributions, withdrawals, and voluntary top-ups. GreatRise IT helps Malaysians make sense of both financial and digital tools.

Have a Specific KWSP Scenario?

Whether you are planning a big withdrawal, voluntary top-up, or switch to Shariah, the GreatRise IT team can help you understand the impact on your dividend.

Related Articles

KWSP Dividen 2026 Announced: 6.15% Rate for 2025 Savings: Full Details, Payout & Easy i-Akaun Guide

Read article

Budget 2026 SME Digitalization Grants: How Sarawak Businesses Can Claim Up to RM500K

Read article